The Federal Reserve has decided to pause on raising rates, breaking a streak of 15 consecutive increases. This change could bring some relief to consumers who have been dealing with higher mortgage, credit card, and loan costs due to the previous rate hikes.

Since the Fed began raising rates in 2022 to combat inflation, the difference in borrowing costs has become significant. The rate for a 30-year mortgage, for example, has increased from 3.2% to 6.8%, resulting in a 50% increase in monthly mortgage payments for a typical $300,000 home. Credit card interest rates have reached record highs of over 20%, and other loans have also become more expensive.

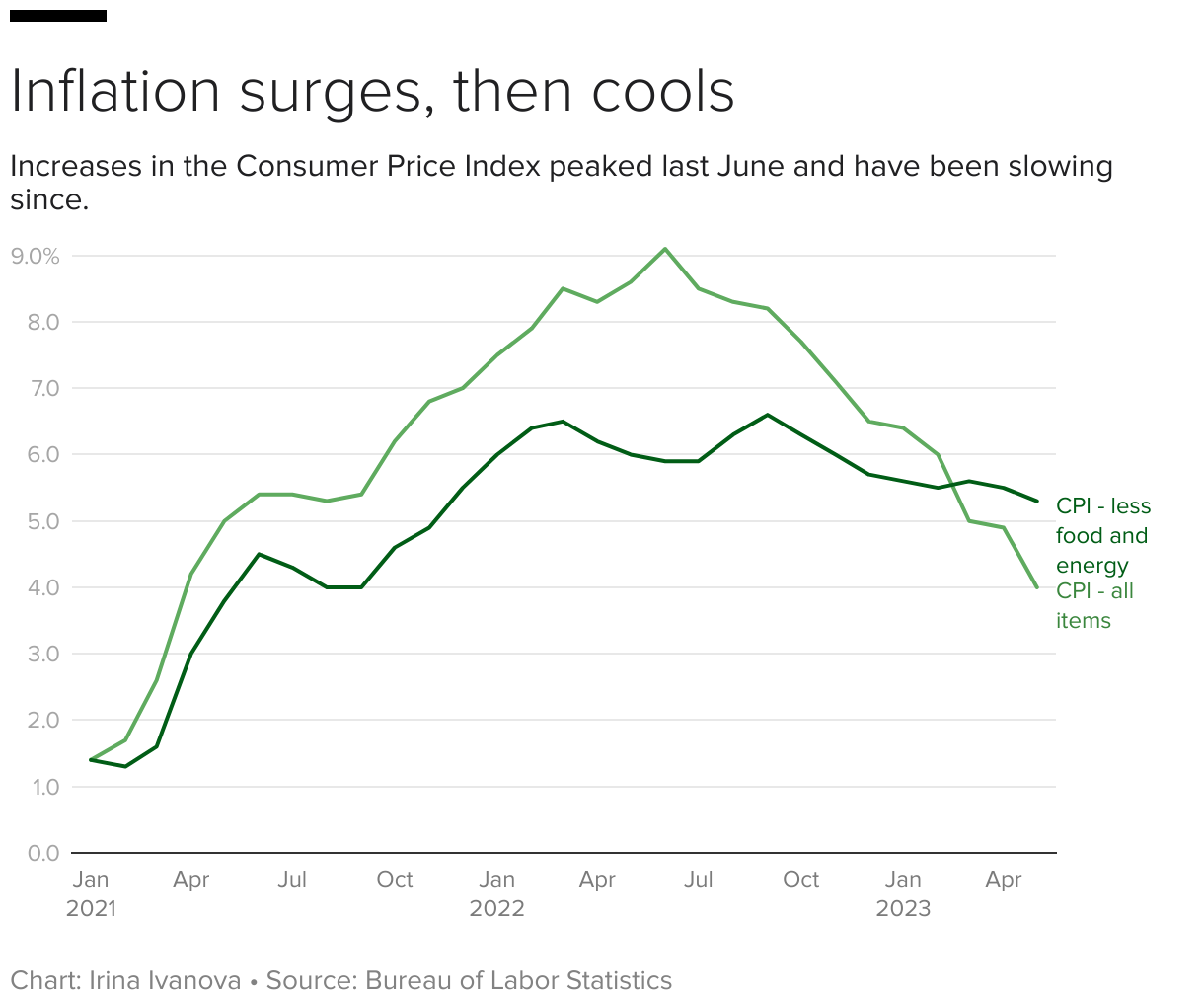

The goal of the rate hikes was to address the highest level of inflation in 40 years. Recent data suggests that these efforts are working, with May’s Consumer Price Index showing the slowest rate of increase in two years. As a result, many economists, including Goldman Sachs analysts, expected the Fed to pause on further rate hikes in order to assess the strength of the economy and avoid tightening too much.

While pausing the rate hikes is a positive development, the damage has already been done, according to Matt Schulz, chief credit analyst at LendingTree. There is still uncertainty about whether this pause will be short-term or long-term.

Here’s how the Fed’s decision to hold interest rates may impact your finances.

Mortgage rates

Mortgage rates are expected to remain steady following the Fed’s pause. This could be beneficial for consumers after the significant increase in home loan costs. Michele Raneri, vice president and head of U.S. research and consulting at TransUnion, predicts that a homebuyer taking out a 30-year loan at the current rate of 6.8% for a $300,000 home would have monthly payments of $1,956. This is a 50% increase from the $1,297 monthly payment in January 2022 when mortgage rates were 3.2%. However, the housing market may still experience fluctuations due to economic uncertainty.

According to Selma Hepp, chief economist at real estate research firm CoreLogic, mortgage rates are likely to remain higher for the remainder of the year, despite gradual declines.

Credit card rates

Consumers with credit card balances are unlikely to see relief anytime soon. LendingTree’s Schulz predicts that APRs could continue to rise, even with the Fed’s pause, as some banks are still incorporating the recent rate hikes into their fee schedules. The typical rate for a new credit card is expected to exceed 24% this month, while APRs on existing credit cards are already close to 21%, the highest since 1994.

Auto loans

Loan rates for new vehicles have remained steady at an average of about 7%, regardless of the Fed’s interest rate decisions. The demand for vehicles and high vehicle prices are more influential factors for auto loan rates. Unless vehicle sales slow significantly, companies and dealers are unlikely to reduce prices or offer better loan rates.

Savings accounts, CDs

Yields on savings accounts and certificates of deposit (CDs) are currently at their highest levels in a decade. However, with the Fed pausing on rate hikes, any further increases in yields may be relatively small. Ken Tumin, a banking expert, expects banks to slow down their deposit rate increases. Despite this, these accounts are still much more rewarding than they were a year ago, with online savings account yields averaging 3.98% and online 12-month CD yields averaging 4.86%.

What’s next for the Fed?

The Fed has hinted at potentially resuming rate hikes later in the year, with a projected final rate of about 5.6%. This suggests two more rate hikes before the end of 2023. This announcement surprised Wall Street, causing stocks to slip. Some experts argue that it’s time for the Fed to stop rate hikes altogether, while others acknowledge that it may take some time to see significant reductions in borrowing costs for consumers.

With reporting by The Associated Press.

Denial of responsibility! VigourTimes is an automatic aggregator of Global media. In each content, the hyperlink to the primary source is specified. All trademarks belong to their rightful owners, and all materials to their authors. For any complaint, please reach us at – [email protected]. We will take necessary action within 24 hours.